Burke CPAs & Advisors

Burke CPAs & Advisors Pro • tem legal solutons

Pro • tem legal solutons Burke Pros

Burke Pros Concentric Wealth Management

Concentric Wealth ManagementQ1/Q2 2025 MARKET REVIEW

Summary

The opening bell of 2025 rang with high hopes, as markets entered the ring expecting strong performance backed by AI breakthroughs, pro-growth policies, and economic momentum. But instead of landing clean shots, the economy found itself on the defensive with President Trump landing a heavy haymaker — a surprise punch in the form of sweeping reciprocal tariffs that have left markets reeling. As the quarter ends and a new one begins, the fight is far from over. Markets, like any good fighter, are assessing the damage, testing mobility, and looking to adjust their stance. With policy uncertainty still throwing punches and economic signals sending mixed messages, investors must stay nimble and be ready to go the distance. Diversification, global exposure, and defensive positioning may prove to be the keys to surviving the next round.

Q1 Summary

The first quarter of 2025 was defined by rising economic and policy uncertainty, mixed data signals, and significant market volatility. Optimism was strong entering the year driven by AI innovation, pro-business hopes, and economic momentum. This quickly gave way to concerns over erratic trade policy, unpredictable fiscal decisions, and fading consumer confidence. Personal income growth accelerated early in the quarter, primarily due to temporary factors like SocialSecurity cost-of-living adjustments and class-action settlements. Meanwhile, consumption was volatile: a sharp January decline was followed by a February rebound. Consumer expectations dropped to near pandemic-era lows by March.

Labor market signals were mixed. Payroll gains held steady through February, but missed the impact of looming government layoffs and private sector job cuts tied to spending reductions. Notably, the broader U-6 unemployment measure spiked to its highest level since 2021.

Policy instability played a central role in market sentiment. Tariff threats and trade policy reversals fueled inflation concerns and discouraged corporate investment. Simultaneously, anticipated pro-growth policies—such as tax cuts and deregulation—have largely stalled. Efforts by the Department ofGovernment Efficiency (DOGE) to aggressively cut federal spending stoked fears over the future of keyprograms, employment, and grants.

Q1 Market Review

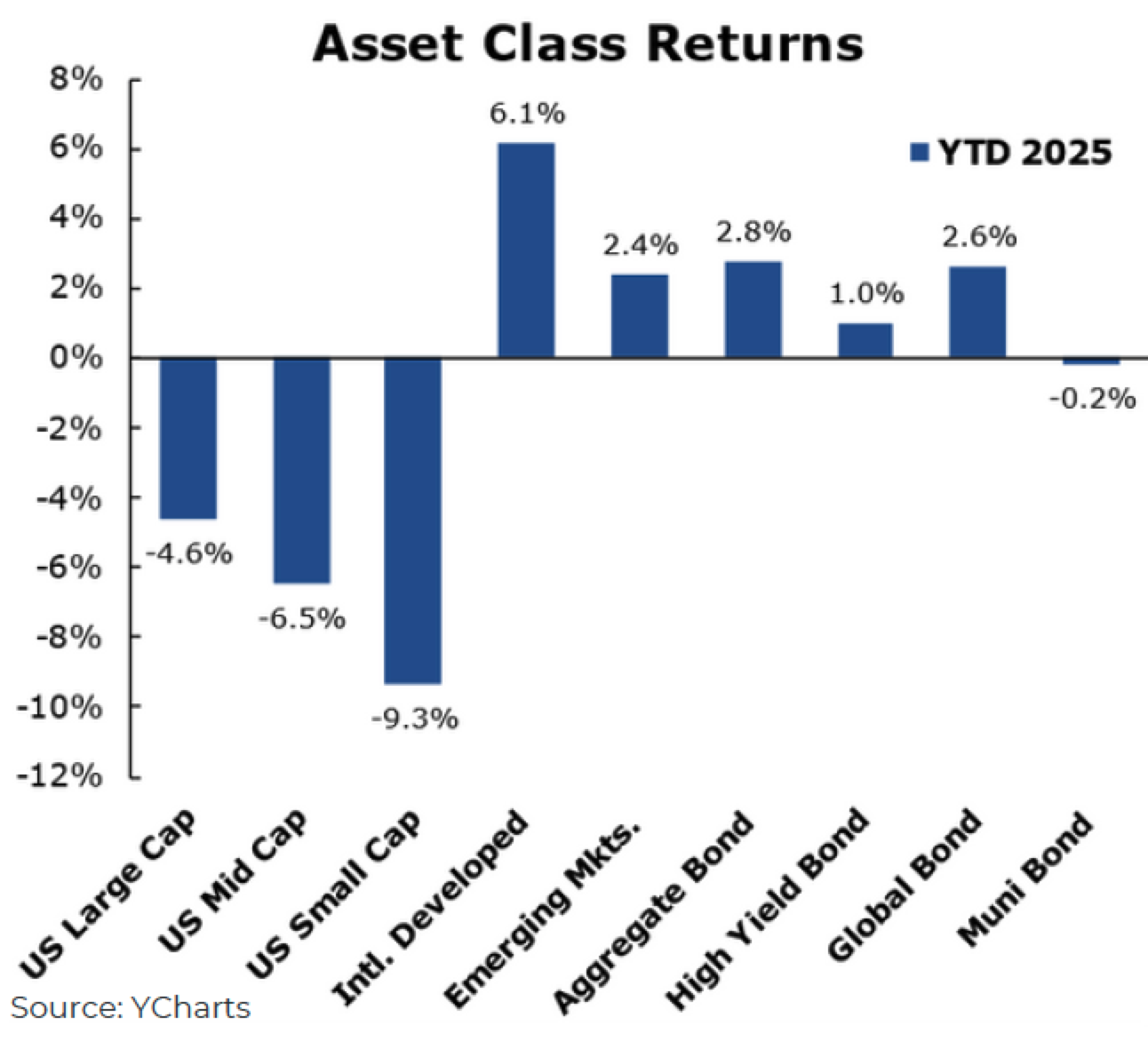

The S&P 500 declined 4.6%, erasing post-election gains. Consumer Discretionary stocks led sector losses, dragged down by falling sentiment and a steep decline in Tesla. Tech and Communication sectorsalso slipped as low-cost AI competitionfrom China weighed on valuations. International equities outperformed U.S. markets by nearly 10 percentage points buoyed by fiscal stimulus in Europe and emerging markets, especially in China. Aweakening U.S. dollar amplified gains for U.S.-based investors. Commodities surged, with copper rising on tariff fears and gold rallying on central bank demand amid geopolitical risk. Bitcoin fell sharply, underperforming after a strong 2024.

Bonds rallied as Treasury yields declined on safe-haven demand. The Fed held rates steady, thoughits projections reflected rising inflation and unemployment risks. Credit spreads widened, indicatingsome level of stress in corporate debt markets.

With economic signals mixed and policy direction unclear, volatility is likely to persist. Tariff policy, government spending cuts, and political gridlock may continue to weigh on business and consumer sentiment. Given that U.S. equities still represent nearly two-thirds of global market capitalization, concentration risk remains elevated. International equities and fixed income strategies appear to be more compelling amidst the uncertain road ahead.

Tariffs: The Background

A seismic shift in global trade policy has been ushered in, with President Trump unleashing what many are calling the most aggressive U.S. tariff regime in modern history. Dubbed “Liberation Day,” the sweeping announcement of reciprocal tariffs has roiled markets, stunned policymakers, and triggered urgent responses around the world. On April 2nd, President Trump declared a national emergency under the International Emergency Economic Powers Act (IEEPA) and revealed a new reciprocal tariff framework. The move establishes a 10% baseline tariff on all imports, with higher rates based on each country’s trade surplus with the U.S. The administration reportedly applied a simple formula which yielded aggressive tariff rates for many key trade partners. So far, it appears that Canada and Mexico are largely exempt due to USMCA. Many industries are bracing for impact, but some items are excluded from the reciprocal tariff structure including gold, pharmaceuticals, semiconductors, critical minerals, and lumber. Auto imports, steel, and aluminum still face 25% duties under separate orders. Tech giants like Apple, Nvidia, Meta, and Tesla have fallen sharply and retail / apparel brands like Nike, Adidas, and Puma have dropped double digits due to their supply chains exposure to Vietnam. U.S. Treasury yields are off as well, with the 10-year hitting floating just above 4.00%. Gold reached a record high price amid chaos and the dollar has fallen sharply reflecting concerns over trade and inflation.

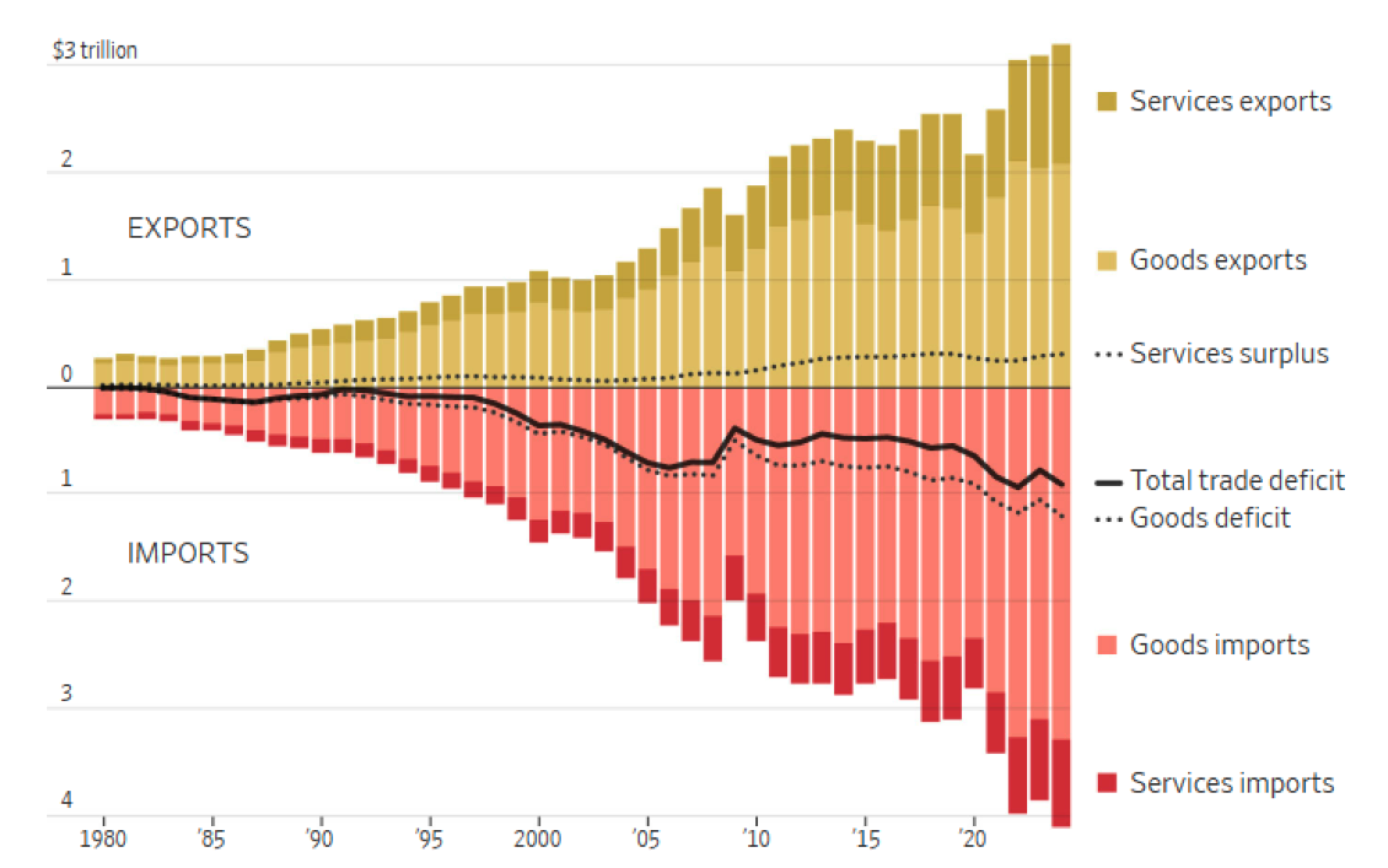

US Trade Balance by Year

Source: Wall Street Journal, Commerce Department

The Potential Impact

Experts are estimating that the GDP hit could be -1 to -1.5%, with +1 to +1.5% upside to inflation. Many are warning of likely escalation from trading partners and additional sectoral tariffs. Fed Governor Adriana Kugler said inflation progress may have stalled and that Tariffs pose an upside risk to inflation, reinforcing the Fed’s current pause on rate cuts.

We urge you to consider that this is a fluid and fast-moving situation, and we are monitoring it closely. Depending on when you are reading this, information may already be outdated. Global trade partners have already begun reacting. China has strongly condemned the tariffs, pledging resolute countermeasures including a 34% tariff on U.S. goods and investigations into U.S. firms like Apple, Tesla, and Starbucks. The European Union is seeking a 4-week window to negotiate and is considering emergency support instead of immediate retaliation. Japan and Vietnam were both caught off-guard by tariff rates far exceeding expectations, though negotiations with Vietnam appear imminent.

Tariffs have the potential to have negative, unintended consequences should there be retaliation from other countries or if consumers and businesses tighten their spending. Tariffs may stimulate growth in Europe and Asia, which could lead to an attractive investment backdrop overseas.

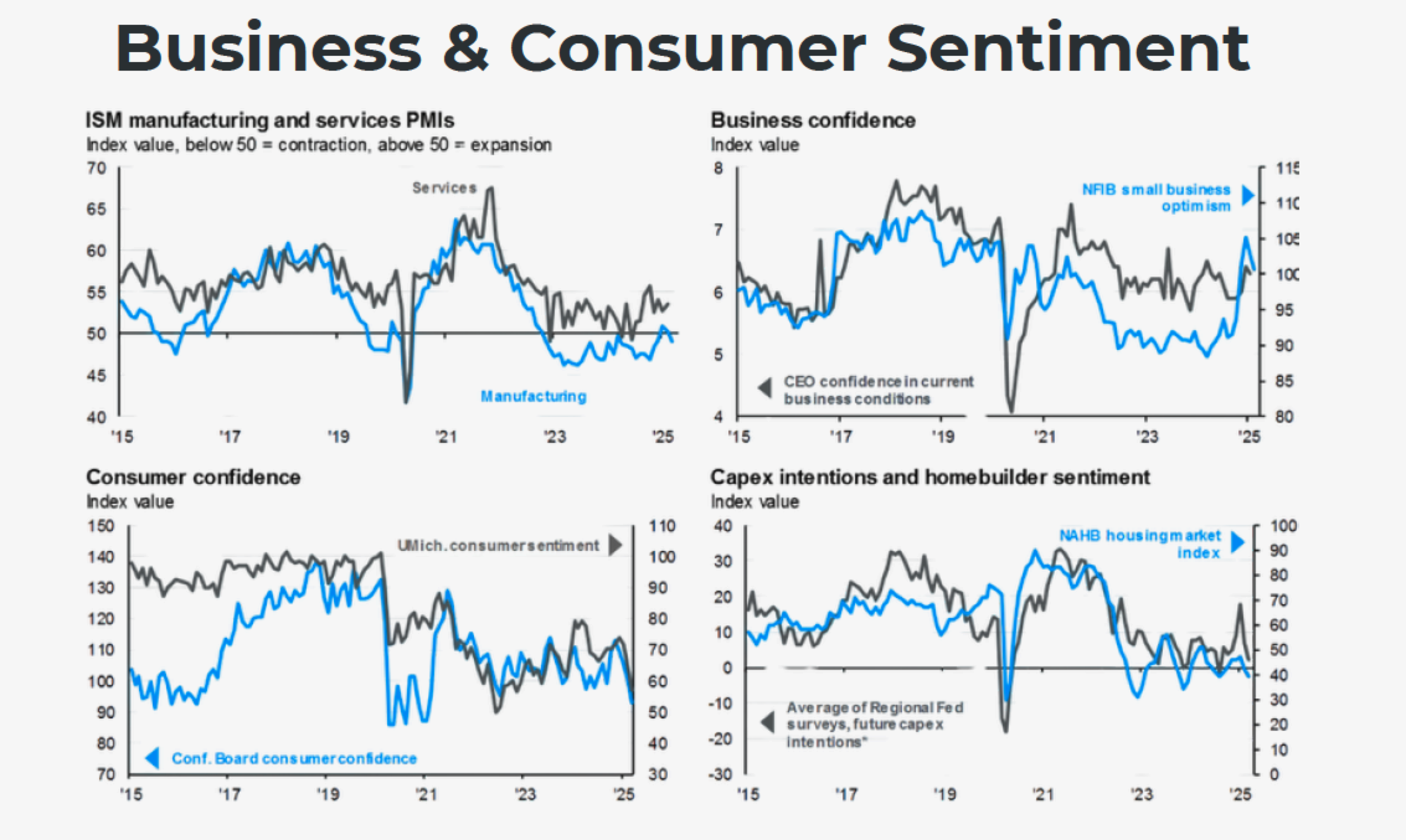

We’re observing a deterioration in business and consumer sentiment amidst policy uncertainty and could indicate a slow down in economic momentum and activity. Though we could see a pick-up of inflation in the short-term, tariffs will likely be deflationary in the long run.

Source: JPMorgan Guide to the Markets

Rationalizing and Realizing

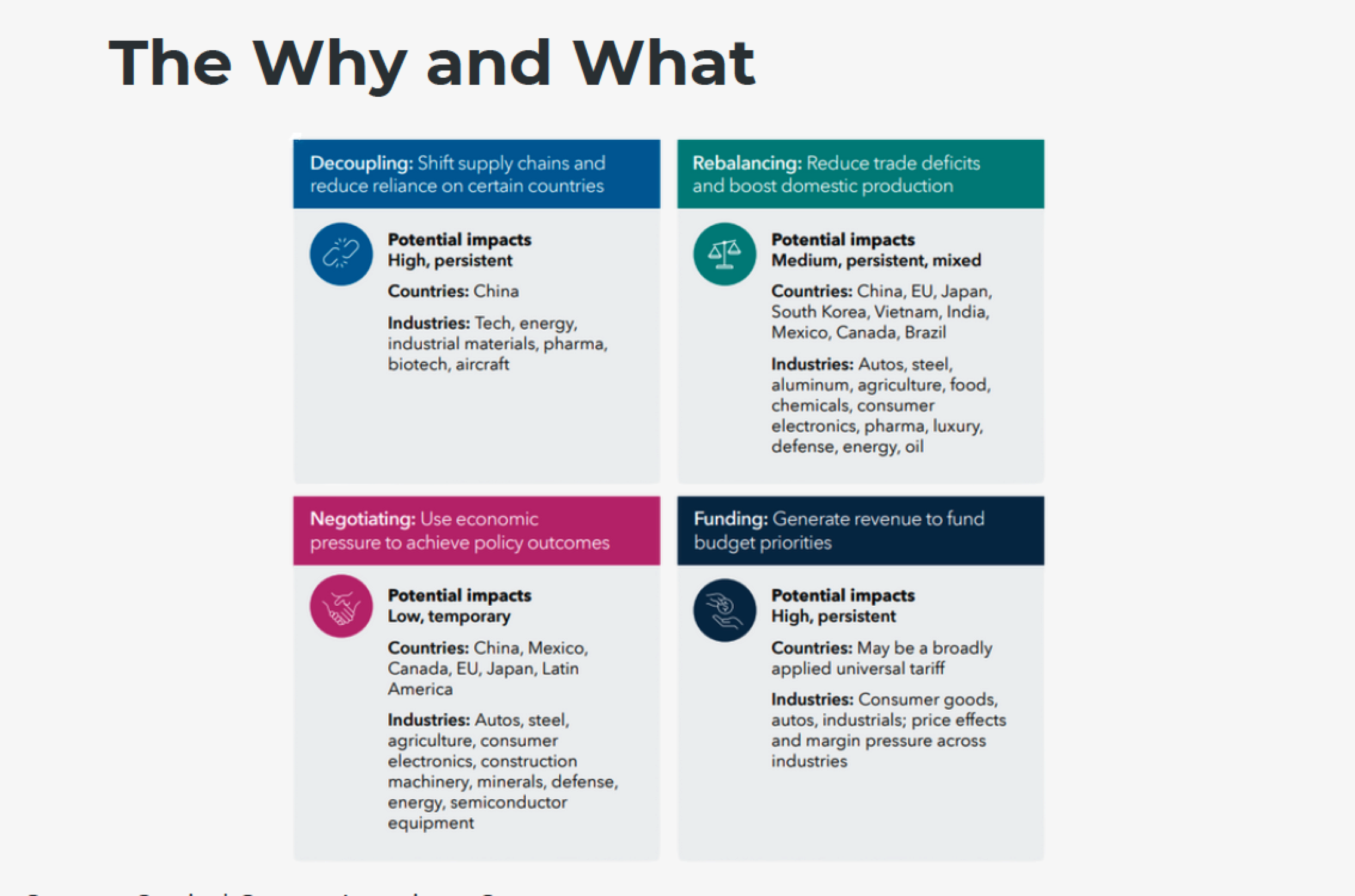

President Trump’s approach blends economic leverage with political messaging and fits into a broader framework of U.S. policy objectives. Overall, his vision goes beyond tariffs—it includes “One Big Beautiful Bill” in Congress including permanent tax cuts, spending reductions, and a debt extension. This is a broader shift in geopolitical alignment, with trade used as a primary weapon of statecraft. Capital Group has published a useful framework to understand the motivations and impacts of tariffs:

Source: Capital Group, American Compass

In Closing

This is not just a blip—it’s a potential rewiring of global trade as we know it. For investors, companies, and policymakers alike, understanding the tariff landscape is now essential. The risk of a full-blown trade war is back. If retaliations mount, the global economy could be pushed toward recession. Yet markets may adjust if negotiations temper the most extreme scenarios. The volatility may persist, but so will the opportunity for those who stay informed and adaptive.

It’s important to remain committed to a long-term plan. We stress that having a balanced asset allocation and a long term focus is crucial to the success of any plan. Though times like this can be unnerving, keeping the course will indeed lead to smooth sailing. long-term

Disclosures

Asset allocation does not assure or guarantee better performance and cannot eliminate the risk of investment losses. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Concentric Wealth Management research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.

When referencing asset class returns or statistics, the following indices are used to represent those asset classes, unless otherwise noted. Each index is unmanaged, and investors can not actually invest directly into an index:

– US Large Cap – S&P 500 Total Return

– US Mid Cap – S&P 400 Total Return

– US Small Cap – S&P 600 Total Return

– International Developed – MSCI EAFE Total Return

– Emerging Markets – MSCI Emerging Markets Total Return

– Aggregate Bond – Bloomberg US Aggregate

– High Yield Bond – Bloomberg US Corporate High Yield

– Global Bond – Bloomberg Global Aggregate

– Municipal Bond – Bloomberg Municipal Bond

Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions. International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions. Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations. Cash may be subject to the loss of principal and over a longer period of time may lose purchasing power due to inflation sector or industry factors, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impacted by currency and/or country specific risks which may result in lower liquidity in some markets. Marketable Alternatives involves higher risk and is suitable only for sophisticated investors. Along with traditional market risks, marketable alternatives are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility or the potential for loss of capital. Additionally, short selling involved certain risks including, but not limited to additional costs, and the potential for unlimited loss on certain short sale positions.

S&P Total Return 500 – Covers the 500 largest companies that are in the United States. These companies can vary across various sectors.

S&P MidCap 400 Total Return Index – A stock market index from S&P Dow Jones Indices. The index serves as a barometer for the U.S. mid-cap equities sector and is the most widely followed mid-cap index.

S&P SmallCap Total Return 600 – Seeks to measure the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

MSCI EAFE Total Return Index – An equity index which captures large and mid-cap representation across 21 Developed Markets countries* around the world, excluding the US and Canada. The index covers approximately 85% of the free float adjusted market capitalization in each country.

MSCI Emerging Markets Total Return Index – Captures large and mid-cap representation across 25 Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

Bloomberg US Aggregate Bond Total Return Index – Used as a benchmark for investment grade bonds within the United States.

Bloomberg US Corporate High Yield Total Return Index – Covers performance for United States high yield corporate bonds. This index serves as an important benchmark for portfolios that include exposure to riskier corporate bonds that might not necessarily be investment grade.

Bloomberg Global Aggregate Total Return Index – Measures the performance of global investment grade fixed income securities. This index is widely used as a benchmark for fixed income securities.

Bloomberg Municipal Total Return Index – Serves as a benchmark for the US municipal bond market. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk.

The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Indexes discussed are unmanaged and you cannot directly invest into an index.

Past performance is not a guarantee of future results.

Securities offered through Avantax Investment Services ℠ , Member: FINRA, SIPC. Investment Advisory services offered through Avantax Advisory Services ℠ Insurance services offered through an Avantax affiliated insurance agency.